Cross-Border Deals Are the New Normal. Direct Investment Is Not Built for Them.

The pace of cross-border deal activity in private markets has accelerated sharply. Syndicate leads in Singapore are co-investing with angels from Dubai. Fund managers in Hong Kong are writing tickets into Southeast Asian startups alongside European family offices. The capital is global. The question is whether the structure keeps up.

For most of that activity, it doesn’t. Direct investment, the practice of each investor taking a direct equity position in the target company, was built for a world where all parties are in the same jurisdiction, operating under the same legal framework, and comfortable signing the same documents. That world is increasingly rare.

When you take a direct investment cross-border, you’re not just executing a deal. You’re navigating a stack of legal, tax, and compliance requirements across multiple jurisdictions simultaneously, and doing it separately for every LP in the round. One deal with twelve international investors is twelve separate compliance processes.

SPVs exist precisely to solve this. They don’t just simplify the structure. They make cross-border execution possible at a speed that direct investment simply cannot match.

The Side-by-Side: Where Direct Investment Breaks Down Globally

Legal Complexity

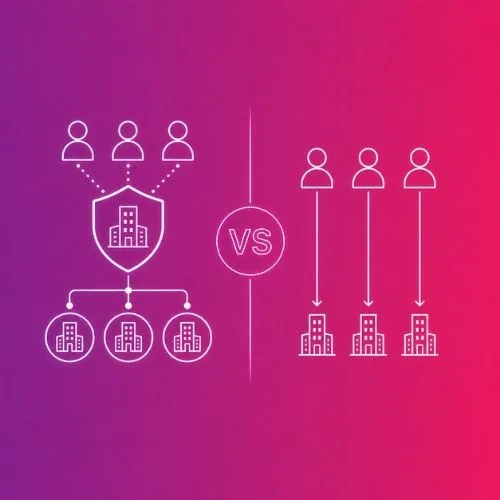

With direct investment, each LP holds equity directly in the portfolio company. That means the cap table reflects every investor’s jurisdiction, entity type, and shareholding structure. For a startup incorporated in, say, the Cayman Islands with LPs from the US, UAE, and Singapore, the legal review required to accommodate each investor’s position directly is significant, slow, and expensive.

With an SPV, there is one investor on the cap table: the SPV itself. All underlying complexity, LP onboarding, KYC, subscription agreements, is handled at the SPV level, invisibly to the portfolio company. The founder sees a clean cap table. The syndicate lead manages one vehicle, not twelve bilateral relationships.

Tax Treatment

Cross-border direct investments trigger a range of withholding tax, capital gains, and reporting obligations that vary by investor jurisdiction. Without careful structuring, LPs can face unexpected tax exposure in both their home jurisdiction and the portfolio company’s domicile.

An SPV, domiciled in an appropriate jurisdiction, can provide a consistent and transparent tax treatment for all LPs, reducing complexity and providing a known tax profile from the moment of investment.

Execution Speed

Direct investment cross-border requires legal review in multiple jurisdictions, separate KYC for each LP at the company level, and bilateral document execution. In practice, this adds weeks to a close, sometimes more. In a competitive deal, that timeline is disqualifying.

An SPV compresses all of that into a single vehicle close. KYC is completed once per LP, documents are executed at the SPV level, and the portfolio company receives one clean wire. A deal that might take six to eight weeks to close directly can close in two to three weeks through a well-structured SPV.

A Real Deal Scenario: $800K into a Series A, 14 LPs Across 6 Countries

Consider a syndicate lead closing an $800K allocation into a Series A round. The LP base spans Singapore, Hong Kong, the UAE, the UK, Germany, and Australia. All 14 LPs are qualified investors, but each brings different KYC requirements, subscription documentation expectations, and tax considerations.

Via direct investment: the portfolio company’s legal team needs to accommodate 14 different investor structures. The round drags. Two LPs miss the deadline because their documents weren’t processed in time. The syndicate lead spends three weeks chasing paperwork instead of managing the relationship.

Via SPV on Auptimate: all 14 LPs onboard through a single digital portal. KYC is completed per investor once. The SPV executes one set of subscription documents with the portfolio company. The close takes 16 days. All 14 LPs participate. The founder receives a single clean entry on their cap table.

The deal is the same. The structure determines whether it closes cleanly or not.

Structure Is Now a Competitive Advantage in Global Deal Execution

In a market where the best deals are competitive and timelines are compressed, the ability to close cleanly and quickly is a differentiator. Syndicate leads who can put a clean SPV vehicle in front of a founder, backed by a properly onboarded LP base, win allocation over leads who are still sorting out cross-border documentation.

Auptimate’s Single Asset SPV is built for exactly this. Global jurisdiction coverage, digital LP onboarding, customisable carry and fee structures, and an LP portal that keeps every investor informed from close to carry, all in one platform.

The World Is Global. Your Deal Structure Should Be Too.

Cross-border investing isn’t a niche strategy. It’s the direction the market is moving. The syndicate leads who build global LP bases and execute cleanly across jurisdictions will have access to deal flow and co-investment relationships that locally-constrained operators simply won’t.

The structural foundation for that is an SPV built for global execution.